Important Disclosures

This is a conceptual example for educational purposes only. All policies are subject to underwriting and approval. Loan values and policy benefits are not guaranteed and depend on actual policy performance. Taking loans from a life insurance policy reduces the death benefit and may cause the policy to lapse if not properly managed. Bank participation is subject to approval. NIW and Kai-Zen are not affiliated with National Life Group.

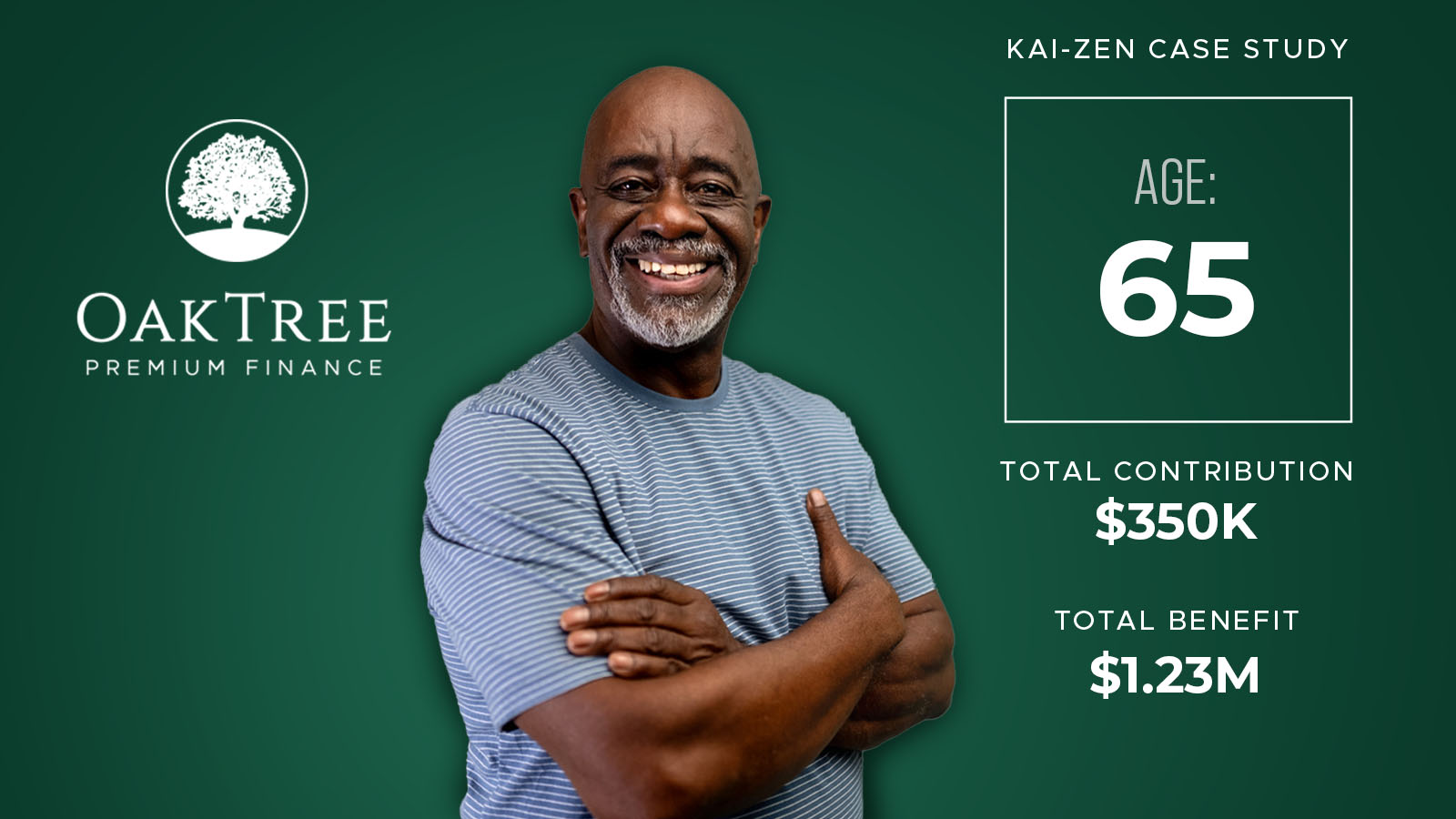

Properly structured life insurance can be more than protection—it can be a tax-smart, multi-purpose financial tool. If you’re thinking about long-term care, retirement income, and legacy planning… Kai-Zen may be worth exploring.

Learn more at https://kaizennlg.simplicityniw.com/3acdd6d2-3a5c-441e-a301-7fefc99afcc5